NIC MAP Q3 Occupancy Results Fall Short Of Expectations

In more normal times, whatever that may be, the third quarter is supposed to be a good one for occupancy increases, perhaps the best quarter of the year. Not so in the past three years, however. NIC MAP has reported yet another slow month for seniors housing occupancy, which does not bode well for the rest of the year or for early 2018. The modest (10 basis points) increase in assisted living occupancy, combined with the modest decrease (-10 basis points) for independent living, does not bode well for the fourth quarter, when recent weather-related events will surely have a negative impact. Following that will be the first quarter flu season problems, which in 2017 lasted well into the... Read More »

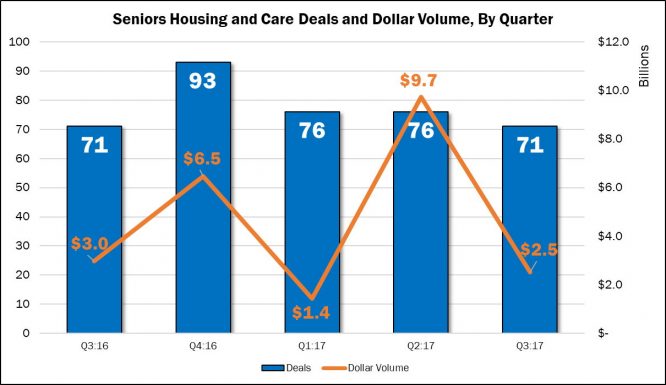

Third Quarter M&A Results Are In

We will be addressing the quarterly seniors housing and care M&A results in both the October issue of The SeniorCare Investor, as well as in our Health Care M&A Quarterly Report, which covers all 13 health care sectors. But, here is a preview: Although it remained above 70 deals for the quarter, seniors housing and care M&A activity fell to a year-low, tying with last year’s third quarter at 71 publicly announced transactions. Dollar volume also fell from its recent peak of $9.7 billion in the second quarter of 2017, recording $2.5 billion in transaction value based on disclosed prices. Increasingly, we have seen buyers prefer the one-off deals that come with one or two... Read More »

Capital One Releases Survey Results

Capital One released its annual survey results from more than 150 senior executives about the 12-month outlook for various issues in seniors housing and skilled nursing. Despite record-high acquisition prices, 37% of the respondents believe acquisitions of existing facilities represent the biggest opportunity, with 30% believing repositioning existing properties represents the best opportunity. In addition, 89% believe the level of M&A activity will remain the same or increase in the next 12 months, split almost equally between the two. Regarding challenges in the next 12 months, 33% cited labor cost pressures and 32% cited supply/demand imbalances. Fewer than 10% were concerned about... Read More »

REIT Financing: RIDEA vs. Sale/Leaseback

During our recent webinar on REIT financing where we discussed the pros and cons of using the more traditional sale/leaseback structure, we posed a few questions to the audience. Let’s just say, the answers surprised us. The first was whether, if choosing REIT financing today, they would prefer the traditional sale/leaseback structure which involves fixed lease payments that increase every year, or the newer RIDEA structure, where they enter into a joint venture with the REIT and manage the properties for the joint venture. We assumed that most people would prefer the RIDEA structure given the nature of the sale/leaseback structure with 2.5% to 3.0% annual escalators. Wrong. A slight... Read More »

What Happens When You Weight A Cap Rate By Beds?

Partly due to historical precedent, we have always presented our cap rate analysis on an unweighted average basis, meaning that the cap rate for a portfolio of facilities would carry the same weight as that of a single 80-bed facility. For those who believe that portfolios will usually command a lower cap rate, then a weighted average would be the most accurate method to determine what is really happening in the market. Even a 200-bed facility acquisition, because of the implied increase in investment risk, should in theory be treated differently from that of a 50-bed rural facility. Consequently, a few years ago we went back and recalculated the cap rates to weight them based on the... Read More »Schedule a demo

Gain access to the best healthcare and long-term care investment intelligence, data, and analysis.