What Happens When You Weight A Cap Rate By Beds?

Partly due to historical precedent, we have always presented our cap rate analysis on an unweighted average basis, meaning that the cap rate for a portfolio of facilities would carry the same weight as that of a single 80-bed facility. For those who believe that portfolios will usually command a lower cap rate, then a weighted average would be the most accurate method to determine what is really happening in the market. Even a 200-bed facility acquisition, because of the implied increase in investment risk, should in theory be treated differently from that of a 50-bed rural facility. Consequently, a few years ago we went back and recalculated the cap rates to weight them based on the... Read More »

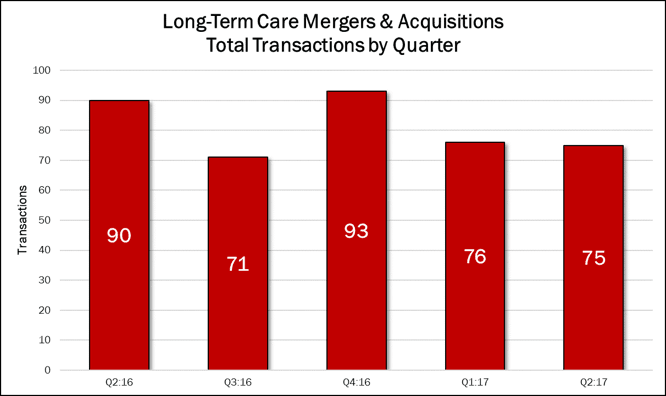

Quarterly Results Are In

If you go by the number of transaction announced from April 1, 2017 to June 30, 2017, the second quarter may seem a bit slow, especially when compared to the recent quarterly highs of 90 deals in the second quarter of last year and of 93 deals in the fourth quarter of 2016. Keep in mind, these are preliminary numbers, as we hear of more transactions as the year goes on. M&A activity stayed virtually even in the second quarter, down 1% over the previous quarter, to 75 transactions. The quarter’s deal volume makes up 24% of the 315 deals announced within the past 12 months. Nothing too drastic there. However, based on revealed prices, approximately $9.7 billion was committed to finance... Read More »

SNF, AL and IL Values All Remain High

For the four quarters ended June 30, 2017, skilled nursing, assisted living and independent living properties remained at or near their all-time high values, while cap rates decreased across the board. A quarter does not make a trend, but across the seniors housing and care spectrum, values have remained stubbornly high. Stubbornly? Skilled nursing values peaked in 2016, while seniors housing peaked in 2014 with a matching peak in 2016. People, including myself, thought that values would slowing decline, especially if interest rates spiked up. Well, neither event has occurred. For the 12 months ended June 30, 2017, skilled nursing average prices posted a small decline to $97,900 per bed... Read More »

What Do The Experts (and the Audience) Say On The Labor Crisis?

On Thursday, July 13, we hosted a webinar entitled, “The Coming Labor Market Shock to Senior Care,” with panelists Glenn Barclay of Quality Senior Living, John Gonzales of SDG Senior Living and Lori Porter of the National Association of Health Care Assistants. For 90 minutes, the panel discussed how the industry will deal with a labor shortage, improving retention rates, improving onboarding and training practices, an increased minimum wage to $15 per hour in the coming years, technology’s impact on labor demands and how middle market operators will be able to deal with these changes. If you’d like to hear a recording of the webinar, click here. Needless the say, the industry has a lot of... Read More »Seniors Housing Occupancy Weakens

NIC announced their second quarter occupancy and development trends, and unfortunately it was not pretty. After a first quarter which suffered from the ubiquitous flu season census declines, we had expected, at worst, a small sequential decline in the second quarter, but perhaps a small 10 to 20 basis point uptick, maybe even better. For majority assisted living in the top 31 MSAs, for those properties open for two years (stabilized properties) average occupancy dropped 50 basis points from the first quarter to 88.9%, but down 80 basis points from the year-ago quarter. Historically, the average second quarter sequential decline is 10 basis points, and the current 50 basis point drop was... Read More »Schedule a demo

Gain access to the best healthcare and long-term care investment intelligence, data, and analysis.