Senior Housing & Care Acquisition Pricing Softens

Across the senior housing and care spectrum, average per-unit and per-bed prices softened a little in the four quarters ended September 30, 2017. I am sure a lot of you have heard that the senior housing acquisition market is soft, reflecting concerns over census and rising costs. But how soft? Not very, according to our recent acquisition data. For the four quarters ended September 30, the average price per unit for assisted living did drop compared with the four quarters ended June 30, but by only 4% to $208,200. It is still higher than the $193,650 per unit for calendar year 2016. The average AL cap rate dropped to 7.9%. The independent living market softened a little as well, with the... Read More »

The Skilled Nursing Investors Speak

On October 12, we hosted a webinar called “Investing in Skilled Nursing Facilities,” where our editor, Steve Monroe, and a panel of experts, including Joseph Deans of Diversicare Healthcare Services, Steve LaForte of Cascadia Healthcare and Talya Nevo-Hacohen of Sabra Health Care REIT, discussed the skilled nursing M&A environment today. That spanned from who is buying SNFs and why, the discrepancy between record-high values and current industry headwinds, and whether SNFs will win the battle against LTACs and IRFs for the post-acute patient, among several other topics. But we also brought in the audience to get their opinion on a few issues too, and here are the results: Do... Read More »NIC MAP Q3 Occupancy Results Fall Short Of Expectations

In more normal times, whatever that may be, the third quarter is supposed to be a good one for occupancy increases, perhaps the best quarter of the year. Not so in the past three years, however. NIC MAP has reported yet another slow month for seniors housing occupancy, which does not bode well for the rest of the year or for early 2018. The modest (10 basis points) increase in assisted living occupancy, combined with the modest decrease (-10 basis points) for independent living, does not bode well for the fourth quarter, when recent weather-related events will surely have a negative impact. Following that will be the first quarter flu season problems, which in 2017 lasted well into the... Read More »

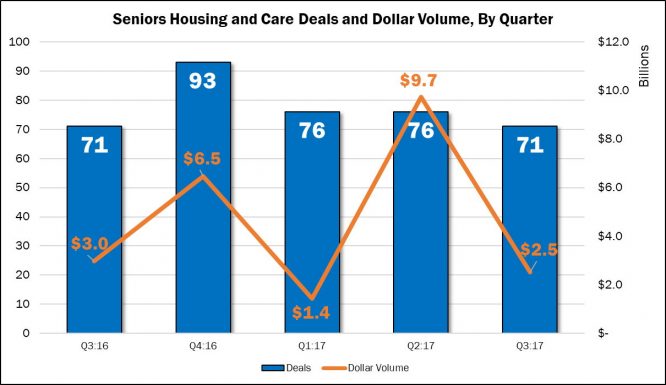

Third Quarter M&A Results Are In

We will be addressing the quarterly seniors housing and care M&A results in both the October issue of The SeniorCare Investor, as well as in our Health Care M&A Quarterly Report, which covers all 13 health care sectors. But, here is a preview: Although it remained above 70 deals for the quarter, seniors housing and care M&A activity fell to a year-low, tying with last year’s third quarter at 71 publicly announced transactions. Dollar volume also fell from its recent peak of $9.7 billion in the second quarter of 2017, recording $2.5 billion in transaction value based on disclosed prices. Increasingly, we have seen buyers prefer the one-off deals that come with one or two... Read More »

Capital One Releases Survey Results

Capital One released its annual survey results from more than 150 senior executives about the 12-month outlook for various issues in seniors housing and skilled nursing. Despite record-high acquisition prices, 37% of the respondents believe acquisitions of existing facilities represent the biggest opportunity, with 30% believing repositioning existing properties represents the best opportunity. In addition, 89% believe the level of M&A activity will remain the same or increase in the next 12 months, split almost equally between the two. Regarding challenges in the next 12 months, 33% cited labor cost pressures and 32% cited supply/demand imbalances. Fewer than 10% were concerned about... Read More »Schedule a demo

Gain access to the best healthcare and long-term care investment intelligence, data, and analysis.