Expense Ratios: Independent Living Vs. Assisted Living

When comparing the independent living and assisted living markets, one would expect IL communities to operate at a higher margin than AL, given its lower services and thus, costs. And while that remained true in 2016, independent living and assisted living expense ratios came as close to equal as any time in the past, at 69.5% and 72.5%, respectively, according to the 22nd Edition of The Senior Care Acquisition Report. Only in 2011, when independent living had a higher expense ratio than assisted living, by just 10 basis points, did the two sectors operate more similarly. The shift has been steady, with the spread between IL and AL expense ratios of properties sold sharply decreasing from... Read More »Expensive Seniors Housing Sales With Low Expense Ratios

It’s no surprise that as a community’s expense ratio declines, its value increases. As such, there was a near-perfect correlation between the expense ratio and the average price per unit paid in the seniors housing market in 2016 (including independent living and assisted living communities), according to the The Senior Care Acquisition Report. The best-operating communities with expense ratios under 65% were valued on average at $298,100 per unit, way up from the $256,100 per unit recorded in 2015. Both years were still heavily influenced by high-quality independent living sales. Meanwhile, the grouping with a 65% to 69% expense ratio fell in value year over year, from $193,000 per unit... Read More »

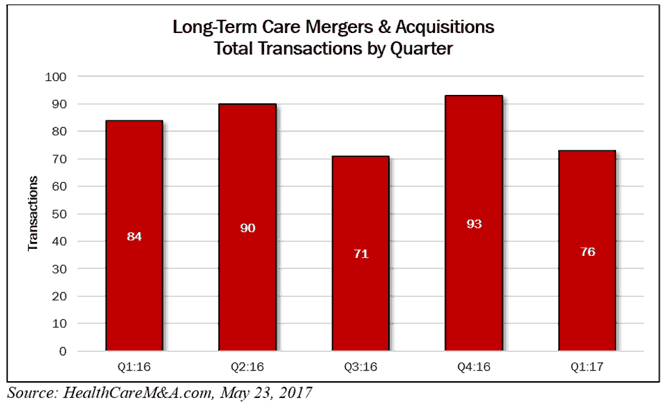

New Senior Care M&A Data

Assisted living per-unit prices rise for the latest four quarters, while skilled nursing remains the same. It was a relatively slow first quarter with regard to publicly announced seniors housing and care acquisitions, other than some old large deals announced last year that finally closed in the quarter. On a rolling four quarters basis, the average price for assisted living jumped to $210,300 per unit for the period ended March 31, compared with $193,650 per unit for calendar year 2016. The average cap rate remained at 8.5% but with an obvious wide range. Meanwhile, independent living did the reverse, dropping to $208,900 per unit for the four quarters ended March 31 compared with... Read More »Sizing Up the Seniors Housing Market

In 2016, buyers paid up for larger seniors housing communities (including independent living and assisted living) compared to 2015. We observed in the 22nd Edition of The Senior Care Acquisition Report that once again, the largest properties, with 150 units or more, still beat out smaller properties in price, averaging $226,200 per unit, 16% higher than 2015’s $195,600 per unit. Here is where the high-priced independent living communities that sold in 2016 exerted their influence in the overall market, representing a clear majority of the largest properties and pushing up the price. Communities with between 100 and 149 units came with a lower price than 50- to 99-unit communities,... Read More »An Optimal Size for Skilled Nursing?

As the skilled nursing market evolves, lengths of stay and occupancy decline, and new entrants like Mainstreet change the way we view skilled nursing/post-acute care facilities, what is the ideal size of facility now? Based on 2016 sales according to the 22nd Edition of The Senior Care Acquisition Report, the average size of skilled nursing facilities sold dropped for the first time in three years to 122 beds, and was closer to the historical norm of 120 beds. That fell from 130 beds in 2015, and is the lowest since 2013, when facilities averaged 121 beds. The smallest facility sold in 2016 was 40 beds, compared with 30 beds in 2015, while the largest facility sold in 2016 was 744 beds,... Read More »Schedule a demo

Gain access to the best healthcare and long-term care investment intelligence, data, and analysis.